CHAPTER 6

Understanding Your Business Finances

To run your business effectively, you need to know how to manage your finances, which will take time, skill and diligence. Although you don’t need to become an accountant, you will need to understand the basics of your business bookkeeping. This will empower you to always know how your business is doing financially and to be able to spot problems if they arise.

Keep Business and Personal Finances Separate

If you mix your personal and business finances in one account, you have no concrete way of knowing if your business is making or losing money. How will you know how much money you have to pay for business expenses and for personal expenses? For example, if you combine your business and personal finances, how will you know if money in your account can be used to purchase a new piece of business equipment? What if you accidentally spent money for a household purchase that was needed to pay a business tax?

Keeping your business and personal finances separate is also important for tax purposes. You need to know what your business income is and what your business expenses are for any given period of time. You will pay federal, state, and local business taxes on your business revenue. With these taxes, you will need to fill out a variety of reports. At the end of the year, you will file your taxes with the IRS. On your return, you cannot combine your business and personal expenses; they must be reported separately. If your personal expenses are paid with your business account, there are tax consequences. If the IRS finds personal expenses being paid through your business, you may face extra taxes and penalties, and government penalties can be large and very costly to you.

If you have to pay an accounting professional to sort your business expenses from your personal expenses, you will pay extra for this service. It might take an accountant two hours to prepare financial statements. Or it could take an accountant eight hours to separate your personal expenses from your business expenses? If your accountant charges $100 an hour, you could end up with an $800 bill if he or she has to separate your finances.

Managing a Business Checking Account

Opening a business checking account is an essential part of keeping your finances separate. A good software program can help you manage your checking account, and your CPA should be able to recommend one.

When you open a business account, work with a financial institution that knows you. If you have registered your business name, open the account in your business name and Employee Identification Number. If you have not registered your business name, you can still open a business checking account in your name. When ordering checks for your business, it is not necessary to buy a big, expensive book with sheets of checks. You may want to order just a small box of duplicate checks and a checkbook register or whatever works best for you to help you keep good records, while keeping costs to a minimum.

You will deposit all the money you make from your business into this account. All the purchases you make for your business should be paid only from your business account. Otherwise, you have to sort through all your personal records to determine which expenses were for business and which were from your household account. If all businesses expenses are paid out of one account, you will clearly know what you have paid, when you paid it and how much you paid. You will also know who has paid you for work by looking in your checkbook register.

Be detailed when recording items in your checkbook register, even as you start up your business. If you pay an attorney, Mr. Franklin, for legal services, write in your register the date, check number, to whom the check was written, the check amount, and in the second line of the register, write what the check was for.

If your business needs money from your household account to pay a bill, write a check out of your personal account and deposit it into your business account. When you make a deposit, keep a record of the date, the amount, and what the deposit was for. This will help you keep track of how much money you have taken from your personal finances to support your business. In addition to your business checking account, you need one credit card for business expenses. You may need to order supplies, equipment or other items over the phone or online. Having one credit card and one credit card statement that shows all your business purchases will help you keep business and personal finances separate.

You will be able to use the information from your checking account and credit card statements so that you know what your business income is, what your expenses are and what is left over. Reconcile, or balance, your checking account statements and credit card statements each month as soon as they arrive. If you do, and you notice an error, financial institutions typically give you 30 days to contact them and correct the error. Reconciling your accounts can save you from costly problems.

Anna is a small-business owner who, while reconciling her business checking account, noticed that her bank had incorrectly taken $10,000 from her account. She contacted her bank about the error; however, because she had caught the error more than 30 days after she received her statement, the bank refused to correct the mistake, and Anna’s business lost $10,000. Although this may seem unfair, the bank stood by its policies.

Keep Track of Your Business Books

As a small-business owner, you need to have a basic understanding about how to manage your business bookkeeping. Although you may hire a bookkeeper, you still need to know bookkeeping basics. A good software program can save you time and make bookkeeping basics easier for you. Always be sure to back up your files so you maintain your records.

Understanding some basics will help you make better decisions about your business now and in the future. This isn’t going to take the place of what a CPA or bookkeeper can do for you. They have important, integral expertise you will use. But when you know where your business stands financially, you will know if it is the right time to make large purchases or if you should wait. Is it time to take advantage of a supply sale? Is it time to expand your business?

Your Chart of Accounts

Every business has something known as a chart of accounts, a document listing all your business accounts.

Your CPA will help you develop the chart of accounts that is specific to your type of business. The accounts listed in your chart of accounts will transfer to your financial statements. Ask your CPA to fully explain the purpose of a chart of accounts and to be patient with you while you learn how to use one. Your business accounts fall into the following categories: assets, liabilities, equity, income and expenses.

Every business has something known as a chart of accounts, a document listing all your business accounts.

Your CPA will help you develop the chart of accounts that is specific to your type of business. The accounts listed in your chart of accounts will transfer to your financial statements. Ask your CPA to fully explain the purpose of a chart of accounts and to be patient with you while you learn how to use one. Your business accounts fall into the following categories: assets, liabilities, equity, income and expenses.

An asset is something of value you own. For your business, your assets will include: your business checking account; a business savings account; any investments you have in your business name; inventory purchased by your business; equipment purchased by your business; property purchased by your business; and vehicles purchased by your business. You might also have other asset accounts specific to your company.

Some of your assets will wear out over time. For example, equipment, vehicles and buildings will lose value. If you purchased some equipment three years ago, that equipment is no longer worth as much. If you had to sell it today, you would not likely receive the price you paid for it. For this reason, you will depreciate your equipment, vehicles and buildings. The account that reflects this is called accumulated depreciation. Accumulated depreciation is subtracted from your equipment, vehicle or building to determine the current value of the asset.

Business liabilities are monies your business owes. For example, if you have a business credit card, any balance on the credit card is a business liability. Other liabilities include taxes you owe but have not paid. If you have employees, you will owe taxes on their behalf, including: state withholding, federal withholding, Social Security for your employee and your company, Medicare for your employee and your company, and federal and statement unemployment. You will also owe money, or incur a liability, on sales tax you have collected but not yet sent to your state. Other liabilities include business loans you have for equipment, a business mortgage, a business vehicle, a business line of credit or any other business loan.

The difference between what you own and what you owe is called your equity. Assets minus liabilities equals equity. Equity is often referred to as owner’s equity if you are the sole owner of your business. It goes by different names for different types of businesses. For a partnership, it is called partners equity. For a Limited Liability Company or LLC, it is called member equity. For a C Corporation, it is called Retained Earnings and, for an S Corporation, it is also called Retained Earnings. Depending on the type of company you are, you may have additional equity accounts. The one equity account all businesses have is the net income/net loss account.

Your chart of accounts will also include income or revenue accounts and expense accounts, and for some businesses, a cost of goods sold. Income or revenue accounts are your sales from products and services. The value of your sales would be reduced by any product returns or service refunds.

If you manufacture a product, you incur a cost to manufacture that product. This is called a cost of goods sold. For example, if you write and sell a book, the income account would be book sales. The cost of goods sold would be what you pay the printer to print the book. If your business has a cost of goods sold, these figures are tracked and reported separately from your income and expenses, but are included in your income and expense statements.

Expense accounts are accounts that categorize the bills that you pay for your business. Common types of expense accounts include advertising, bank service fees, insurance, interest on loans, outside services, payroll (if you have employees), fees paid to accountants and attorneys, rent, repairs for equipment, supplies (office and shop), telephone travel and utilities.

A business expense is an expense related to operating your business. Some expenses related to your business are tax deductible. Talk to your accountant to find out specifically what you can deduct as your business expenses. Although an item may be tax deductible, that does not mean you can deduct the expense directly from your tax bill. What tax deductible means is the expense is related to operating your business, but it is an expense that is taken away from your income. If you don’t have any income, then you have a loss. The burden of proof is on you to show that your business expenses truly are business expenses in the event of a tax audit.

Mileage and travel are examples of business expenses. If you have to run errands or have appointments outside your office, documentation is critical. When you get into your vehicle, write down your odometer reading. And when you return, before you turn off your vehicle, write down your odometer reading. It is a good idea to have a small notebook or pocket calendar that stays in your vehicle. Keep it clipped to your visor or in your glove compartment or a compartment you have for storage.

Without a written record of odometer readings and your destination, you cannot claim mileage as a business expense. All business-related mileage needs to be tracked so that it can be calculated at the current mileage rate and be deducted on your taxes or be reimbursed through your company if you are incorporated. While you are out, you may incur expenses that are business-related. You may have

lunch with a client or prospective client, or you may have lodging if you traveled to see a client. Toll fees, taxis, buses, airfare, lodging and meals that are business-related should be tracked.

You want to be able to claim all your legitimate expenses at the end of the year. Without records, you will have spent money and time but you will be unable to use the deduction in your business. This means you may have to pay extra taxes on income you make. You want to take advantage of all deductible travel expenses.

IRS publication 334, Tax Guide for Small Business, explains which items must be counted as income, and which can be considered business expenses. The publication can be found at www.irs.gov/publications/p334/index.html.

Sample Simplified Chart of Accounts

Liabilities

Equity

Revenue

Cost of Goods Sold Advertising (brochures, newspaper, radio/TV, telephone book, web site) |

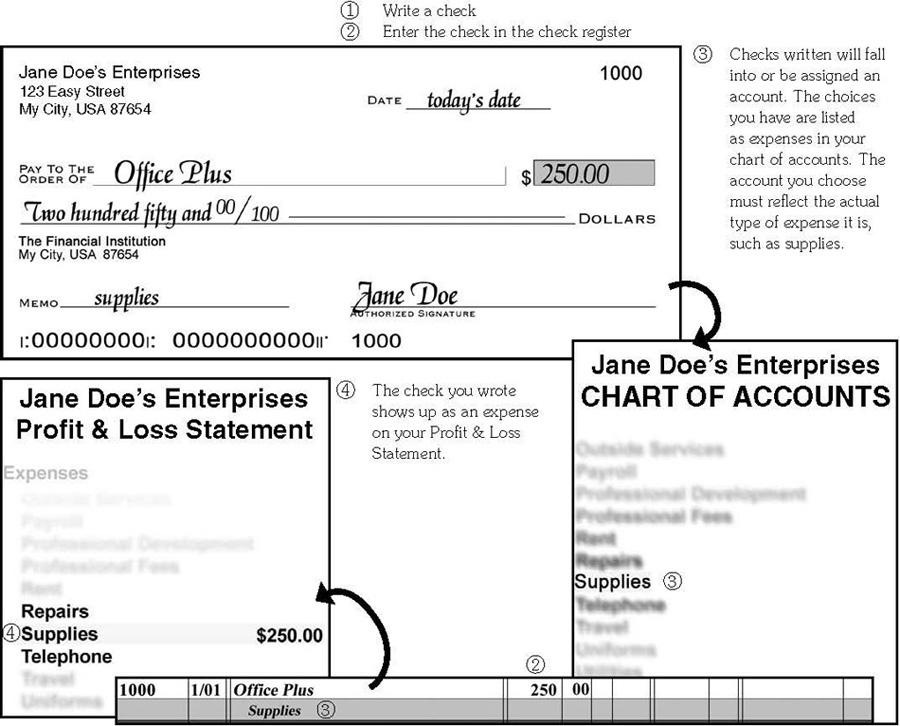

The following example shows what happens when you write a business check. The check is assigned an expense account, such as supplies, from your chart of accounts that indicates the purpose of the check. The expense is reflected in your profit and loss statement.

In addition to a chart of accounts, you will also have a profit and loss statement. A profit and loss statement reflects whether you made or lost money for a specific period of time. This period of time may be a month, a quarter, or a year. Your profit and loss statement lists your sales, minus your cost of goods sold (if you have any), minus your expenses. If your sales are greater than your expenses, you will have a positive number or net income at the bottom of the statement. If your sales are less than your expenses for the period, you will have a negative number or a net loss. Your net profit or net loss is the one figure from your profit and loss statement that is also reflected on your balance sheet.

Sample Simplified Profit and Loss Statement

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Click to download a copy of the above as either a Microsoft Excel worksheet or CSV document.

A balance sheet will list all your business assets, minus all your business liabilities, and your equity on a specific date. The one figure on the balance sheet that comes from your profit and loss statement is your net profit or net loss. This is listed in the equity section of your balance sheet. For business owners, a balance sheet is a snapshot in time about the state of their business. It can change dramatically from one day to the next.

Sample Balance Sheet Assets Liabilities Equity When you add total assets, subtract total liabilities, and subtract total equity you should have a 0 (zero) balance. |

Click to download a copy of the above as either a Microsoft Excel worksheet or CSV document.

When to See Your Accountant

Visiting your certified public accountant on a regular basis will help you understand how your business is doing financially. Plan to see your CPA at least three times a year so he or she can look over your finances.

- June — Have your CPA evaluate and review what has happened in the first six months of the year. Your accountant will catch problems, and you will have time to make adjustments.

- September — Have your CPA review the changes that he or she suggested that you make in June, making sure everything is progressing smoothly.

- February — Submit reports to your CPA for preparation of year-end taxes.

This meeting schedule is based on your fiscal year ending December 31. These meetings don’t have to last more than 15 to 30 minutes. Write a list of questions before your scheduled appointments, and schedule enough time to make sure you get your questions answered. Many certified accountants won’t charge a hefty fee if they know you want just a few minutes of their time and they don’t have to research the answers to your questions.

Preparing a Business Budget

Just as your personal budget guides you in paying for what you need and saving for goals you want to achieve what you want, your business budget will help you reach your business goals. Your business budget will show you whether you are ahead of or behind your planned sales. This is important to know so you can take the appropriate action. Do you need to work harder to increase sales? Are sales growing to the point that you need to increase your production? Are your expenses above or below what you projected? If your expenses are higher, is it because your sales are higher? Or are your expenses higher, and you need to find a way to make cuts? Are your expenses lower than anticipated, and do you have the funds to purchase some additional equipment or a vehicle?

You will develop your budget for a year and then break it down by month. Review your actual income and expenses with your budgeted income and expenses on a monthly basis. If you are off track, you will want to make changes before you run into trouble.

Before working on your business budget figures, you need to know what you want to accomplish:

- How many sales do you want to reach?

- How much growth do you anticipate?

- What do you anticipate it will cost to reach these?

- Will you need to purchase or replace equipment to do this?

- Can you do all this work yourself or will you need help?

Take the accounts listed on your Profit and Loss Statement and list them in the first column of a spreadsheet. In the column, list January and the year, in the next column list February and the year, and so on. The column after December should say Total.

Next, you need to project your income and your expenses. Be sure to take into account the direct and indirect expenses associated with your products and services. When you bid a contract, you will know how many hours you need to do the job and how many supplies you will need. Be sure to add in other costs you incur monthly, such as overhead or indirect expenses of running your business. These might include rent and utilities. Overhead or indirect expenses need to be factored into your costs. That is why you budget for all your expenses.

Simplified Sample Budget

|

Click to download a copy of the above as either a Microsoft Excel worksheet or CSV document.

Cash Flow Statement

A Cash Flow Statement shows the sources of a company’s cash and how it was spent over a specified period of time. It is possible for a company to show a profit on a Profit and Loss Statement but still go out of business because it does not have enough money to pay bills. For example, if you purchase too much inventory and use up all your cash, what will you do if your inventory doesn’t sell as quickly as you believed it would? How will you pay for your monthly expenses? A small business owner needs to be aware of his or her cash flow at all times.

Cash Flow Statements can vary in format. The larger the business, the more varied its sources of cash may be. Lenders often want to see your Cash Flow Statement. They want to know that you will be able to make monthly payments to pay back any loans.

The Cash Flow Statement starts with the net income after taxes from your Profit and Loss Statement. Then you add back any depreciation, because depreciation is a non-cash item and the Cash Flow Statement is about cash. If you have a decrease in your accounts receivables inventory or other current assets, the change is added to your net income. A decrease in your receivables means you have done a better job of collecting the money. If you have an increase in accounts receivable, inventory or other current assets, that means your cash isn’t growing but your non-cash accounts are growing. Therefore that causes a decrease to your cash flow.

If this seems confusing, the following diagram may illustrate your Cash Flow Statement better. A Cash Flow Statement is something your CPA can prepare for you. It is important to keep enough cash to keep your business operating. Do not confuse a Cash Flow Statement with a Profit and Loss Statement or a Balance Sheet Statement. A Balance Sheet tells you the financial position your business is in on a certain date, and a Profit and Loss Statement tells you if your business made a profit or a loss over a specific period. A Cash Flow Statement strictly covers cash and tells you if your cash is increasing or decreasing.

Sample Operating Cash Flow Statement Net Income after tax Investing Cash Flow Financing Cash Flow Cash at the beginning of the period |

A much quicker comparison you can make to check your cash position is one that lenders and CPAs like to use. It is a ratio that is the total of your cash to your short-term obligations. A ratio of 1 to 1 indicates your business is able to pay its short-term obligations with cash. For example, if you had $10,000 in your checking account and nearly $10,000 in short-term bills, you would have a ratio of 1 to 1, or enough cash so that you should be able to pay your bills. However, if you have $10,000 in your checking account but $20,000 in short-term obligations, your business has a 1 to 2 ratio, and you may have difficulties paying your bills.

Businesses have different cash flow cycles. For example, a retailer uses his or her cash to purchase inventory. The inventory goes on the shelves, is sold and the money is collected. This entire cash flow cycle can happen within 30 days. A home builder’s business has a different life cycle. The builder has cash and purchases building supplies. These supplies are used to build a home. After a home is built, it can be sold. The buyer has time to get financing. At the closing date, the builder finally gets paid. This cash flow cycle often lasts six months or more.

Tips to Improve Cash Flow

There are ways to improve your cash flow if necessary. You can sell your product or service and require payment by cash or credit cards rather than allowing the person or business to pay for the product or service next month or at some other time in the future.

If you are having trouble collecting on invoices owed you, you may actively need to contact your accounts to collect on them. Consider requiring a retainer from customers who are slow to pay.

- Add late fees and interest on your accounts when they are not paid as agreed. (Make sure you follow state laws when instituting this policy.)

- Reduce the amount you keep in inventory. You need to have enough to fill demand, but don’t keep months and months of inventory in stock.

- Consider leasing equipment rather than purchasing it.

- For large purchases such as equipment, consider borrowing money for them rather than paying cash.

- Don’t purchase excess supplies. Plan your purchases carefully.

- Don’t pay your bills early. Pay your bills on your due date unless there is a discount for early payment.

- Send invoices out immediately after service rather than waiting until the end of the month.

- Consider using a line of credit to supplement cash if you have a business with a cash flow cycle that takes longer than 30 days.

Internal Controls Protect Your Business

When you understand your business finances, you are better able to identify possible problems. You will know, for example, when you paid for equipment that never arrived. Or, unfortunately, you may discover an employee is stealing from you. Knowing how to read and make sense of your business’ financial statements empowers you to cope with issues that arise. Accounting and bookkeeping should never be taken lightly. Business owners often trust employees with their goods and money but don’t think about the possibility of theft. Nevertheless, as Steve discovered, theft and embezzlement are common.

Steve is a business owner who decided he needed to better understand his business finances and the work his bookkeeper was doing. So when he was in the office by himself, he began going through the office files. He discovered federal forms with levy notices that had never been opened. He found some bills had been paid multiple times, but others had gone unpaid. He also found duplicate files and unopened bank statements. When he reviewed his bank statements, Steve discovered that the funds in his savings account were gone and his checking account was overdrawn. Worse yet, he discovered that his bookkeeper had been stealing from him.

Steve is a business owner who decided he needed to better understand his business finances and the work his bookkeeper was doing. So when he was in the office by himself, he began going through the office files. He discovered federal forms with levy notices that had never been opened. He found some bills had been paid multiple times, but others had gone unpaid. He also found duplicate files and unopened bank statements. When he reviewed his bank statements, Steve discovered that the funds in his savings account were gone and his checking account was overdrawn. Worse yet, he discovered that his bookkeeper had been stealing from him.

Because his bookkeeper picked up the mail every day and kept his books, Steve was unaware there were any problems. To correct the problems, he established some internal controls. He reorganized the filing and bookkeeping system. Steve now spends a few hours each day doing his own books, picking up his own mail and making his own deposits.

Setting up internal controls is a key part of setting up your business. Internal controls are necessary to help your business run smoothly, ensure your financial statements are accurate and reliable, and see that your business complies with laws and regulations. Internal controls should cover the areas that pose the most risk for businesses: cash deposits and checks written, payroll, customer invoicing, collection and credits, and purchasing and storing equipment, supplies and inventory.

At best, internal controls allow for what is called a separation of duties. This means that no individual — except for the owner — is given authority to write and sign checks, make deposits, balance bank statements, take care of all inventory and equipment, bill customers, record payments, and purchase supplies. In a properly developed internal control system, you should not give just one person access to all your business assets and all related accounting records that affect your business. For example, do not allow the same employee who sends customer invoices to also record the payments for those invoices and then make the entries in the accounting system. If one employee handles all these functions, the company is at much greater risk than if these duties are separated among various employees. Whenever practical and possible, two or more employees should authorize, document and record business transactions. Fraud and other illegal activities are more difficult to conceal if two or more people are responsible for these duties.

Internal controls offer protection, not only for you as a business owner, but for your employees. Internal controls can help prevent or help catch mistakes. For instance, if two employees record business transactions and one makes an error, the other may be able to note the mistake and correct it.

Monitor your bank accounts. Have all bank statements sent to your home, not to your business. Do not let someone else, such as your bookkeepers, open your bank statements before you see them. Balance your bank statements within 30 days — preferably within two weeks of receipt. If someone else balances your business accounts for you, review all cancelled checks (or copies) and deposits.

As the business owner, you should sign all checks. Set up a system that requires an invoice to accompany every check. This will help you be aware of all business expenses, and can help you avoid mistakes such as paying bills twice. Do not purchase a stamp of your signature unless you keep the stamp locked up and you are the only one who uses it.

Make your own business bank deposits every day. Keep track of checks, money orders, and cash so they don’t get lost or stolen. If you lose checks, you will have to ask your customers to reissue payments. A customer may do this once, but if he has to do it more than once, he will begin to question how efficiently your business operates and whether or not he wants to do business with you again. As your business grows, you may need to allow other employees to make deposits, but in the beginning, make your own deposits.

Don’t allow the same person who sends invoices to record bad debts. A bad debt occurs when someone owes you money but does not pay you. Leave this kind of entry for your accountant. Your accountant will be able to verify that the account is uncollectible.

Keep all voided checks; do not tear them up. If a check is lost in the mail, you need to require some kind of verification before allowing a check to be reissued.

Maintain a list of all your office equipment. Review your records, and also take a physical count of what and how much equipment you have. Keeping good, up-to-date records can help prevent loss or theft of valuable equipment.

Check your inventory and keep records of what and how much you have. Every year, businesses lose thousands of dollars because employees take business’ supplies and inventory. By keeping good records, you will know what you have and will know when or if items are missing.

If you have employees, set a code of conduct. Don’t allow employees to purchase items from a vendor at a higher price in exchange for some kind of personal reward or perk. When making large purchases, seek at least two or three written bids to make sure you are getting the best possible deal. Don’t allow employees to permit special favors for their friends or purposely overbill customers — both will hurt your business reputation. Encourage employees to report suspicions of fraud.

Require all employees to take a week’s vacation at one time. The person filling in for the employee on vacation should be able to see if the employee on vacation is doing things according to your rules.

Have an accounting firm audit your business. Although you may think you cannot afford an audit, an audit can protect you. You can’t afford to have someone stealing from you. When employees know their work will be audited, they are less likely to try to steal from you.

You are working hard to start your business, and as a self-employed person, you must protect it. The best thing you can do for yourself and your company is to keep your business finances in order and stay in full control of them. To make sure you are fully aware of what is happening with your business finances, make sure you have set up internal controls for your business, and ask yourself the following questions:

- Do I know my daily checking account balance?

- Do I require my bank statements and credit card statements to be reconciled immediately upon their arrivals?

- Do I require financial reports upon reconciliation?

- Do I verify that my cancelled checks and cancelled deposits match my bank statements? Do the checks and deposits reflect accurate amounts? (For example, is a check for $40 being cleared through your account for $400? Watch for evidence of forgery.)

- Do I know how much money I owe and to whom?

- Do I know how much money others owe me? Do I know how long it has been owed?

- Do I scan my paid bills to make sure I’m not overpaying or paying them twice?

- Do I scan my paid invoices to see if they are actually paid and the cash has been deposited?

- Do I regularly check time cards and leave records? Do I use a time clock or written time sheets? Do I verify these records?

- Do I have a scheduled time to do inventory of supplies, equipment, finished goods, inventoried for-sale items, raw goods, work in progress? Do I conduct spot check inventories unannounced?

- Do I have my business bank statements sent to my home so that I am the first one to read them before they go to a bookkeeper?

- Do I pick up and open my own mail before filing it or giving it to a bookkeeper? Am I aware of which bills have been paid, which haven’t and which might have been paid more than once?

- Do I personally take cash deposits to the bank? Do I match the deposit slips to the bank-issued deposit register?

- Am I the only one allowed to sign checks?

Accurate, up-to-date financial records will also help you if problems should arise. Being disorganized makes you a target for crime. Here are some signs that your employees may be putting your business in jeopardy.

- Employees refusing to take vacations and refusing promotions, or acting protective and resistant to change.

- Employees have sudden changes in their lifestyle that can’t be explained (for example, they are driving a new car they can’t afford.)

- Bounced business checks when you know the funds should be there.

- Unusual write-offs being attributed to bad debt.

- Your bookkeeper wants to take the books home to get caught up.

- You have a bad feeling that something is wrong but you can’t identify what it is.

- Things aren’t getting done or just aren’t adding up.

After you get your business finances in order, you will know how much you can invest in setting up your office or shop. In the next chapter, you will learn more about getting your business organized.

“You can either modify your dreams or magnify your skills.” - Jim Rohn, entrepreneur, business philosopher, author and personal development expert

Action Steps

| To Do |

|

![]()

I HAVE READ AND UNDERSTAND THIS CHAPTER:

NO |

YES |

|

Take me back to: |

Take me to: |